- 1 1. What Is an RSI Strategy in MQL5?

- 2 2. How to Implement an RSI Strategy in MQL5

- 3 3. How an RSI Strategy Works

- 4 4. Differences Between an RSI Strategy and Other Methods

- 5 5. Common Mistakes and Cautions

- 6 6. Practical Use Cases

- 7 7. Frequently Asked Questions (FAQ)

- 7.1 7.1 What Is the Best RSI Period?

- 7.2 7.2 Can RSI Be Used Alone?

- 7.3 7.3 Are RSI 30/70 Levels Fixed?

- 7.4 7.4 What Is the Difference Between RSI and MACD?

- 7.5 7.5 In What Markets Does RSI Not Work?

- 7.6 7.6 Is Backtesting Enough?

- 7.7 7.7 Can RSI Be Used for Scalping?

- 7.8 7.8 Is RSI or Bollinger Bands Better?

1. What Is an RSI Strategy in MQL5?

Conclusion:

An RSI strategy is a simple automated trading logic that uses RSI values as conditions for buy and sell decisions.

In MQL5, you can build reproducible entry decisions by using iRSI and CopyBuffer.

1.1 What Is RSI?

Conclusion:

RSI is an indicator that converts the strength of price rises and falls into a number, then helps judge whether the market is overbought or oversold.

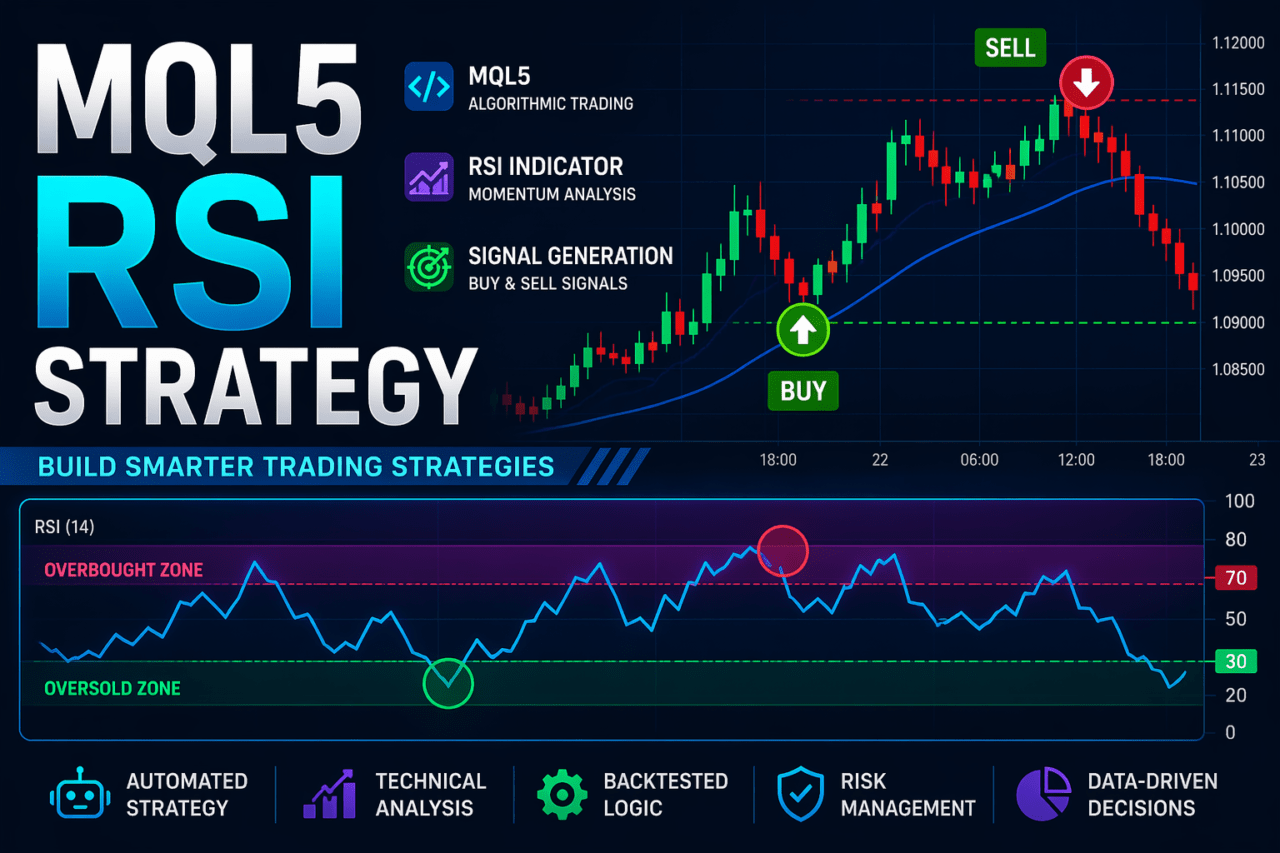

Definition:

RSI, or Relative Strength Index, is an oscillator indicator that shows market strength on a scale from 0 to 100 based on price movement over a set period.

RSI is mainly interpreted as follows.

- RSI > 70: overbought, meaning the market may have risen too far and could fall

- RSI < 30: oversold, meaning the market may have fallen too far and could rise

The basic idea of an RSI strategy is to target a reversal from this overextended state.

The key point is that RSI is an indicator of market condition, not direction.

In other words, it measures an overheated state rather than trend strength.

1.2 The Role of RSI in MQL5

Conclusion:

In MQL5, RSI is handled as numerical data used to generate trading signals.

In MQL5, RSI is not only a display indicator. It is used as a logic component inside an EA, or Expert Advisor.

Its main roles are as follows.

- Judging entry conditions

- Applying filter conditions, such as trading only when RSI is within a certain range

- Managing positions, such as deciding whether to close during overheated conditions

The implementation flow is as follows.

- Create an indicator handle with iRSI

- Get RSI values with CopyBuffer

- Use if statements to judge buy and sell conditions

The important point is that RSI is a real-time value that changes continuously,

and live results can change because of execution, slippage, and spread.

So, “the condition was met” does not mean “profit is guaranteed.”

It is a signal affected by market conditions and order conditions.

1.3 Basic Structure of an RSI Strategy

Conclusion:

An RSI strategy is built with a very simple structure: numerical condition to trading decision.

The basic logic looks like this.

- RSI < 30 -> Buy

- RSI > 70 -> Sell

In MQL5, this can be expressed conceptually as follows.

if(rsi_value < 30)

{

// Buy condition

}

if(rsi_value > 70)

{

// Sell condition

}

In real development, the following extensions are usually added.

- Cross detection, such as the moment RSI crosses up from 29 to 31

- Filter conditions, such as trend and trading session

- Risk controls, such as lot size and stop loss

One caution is that RSI-only conditions often produce false signals.

In particular, during trending markets, RSI can remain pinned at an extreme level.

Common mistakes:

- Entering trades with RSI alone and suffering repeated losses

- Making decisions based only on historical testing, or backtesting

- Ignoring spread and execution

For practical use, it is standard to combine RSI with:

- Trend filters, such as MA

- Volatility adjustment, such as ATR

RSI is not realistically a complete standalone strategy.

It is better viewed as one component that should be used as part of a strategy.

2. How to Implement an RSI Strategy in MQL5

Conclusion:

The flow for implementing an RSI strategy in MQL5 has four steps: create RSI, get values, judge conditions, and execute orders.

By following this order, even beginners can build a reproducible EA.

2.1 Overall Implementation Flow

Conclusion:

First, understand the full processing flow. Once you understand the structure, the code becomes a matter of assembly.

Basic flow of an RSI strategy:

- Create the indicator with iRSI

- Get data with CopyBuffer

- Judge conditions with if statements

- Execute orders with OrderSend

Pseudo flow:

OnTick()

{

// 1. Get RSI

// 2. Check values

// 3. Condition is met

// 4. Place order

}

Important points:

- OnTick runs every time the price updates

- You need to prevent excessive entries, as explained later

- Results change depending on execution timing

2.2 Creating the RSI Indicator with iRSI

Conclusion:

RSI is created as a handle with the iRSI function, and the values are retrieved afterward.

Basic syntax:

int rsi_handle;

rsi_handle = iRSI(_Symbol, PERIOD_CURRENT, 14, PRICE_CLOSE);

Parameter explanation:

- _Symbol: currency pair

- PERIOD_CURRENT: current timeframe

- 14: period, the default setting

- PRICE_CLOSE: based on closing prices

Cautions:

- Create the handle in OnInit as a basic rule

- Creating it on every tick worsens performance

- Always check for INVALID_HANDLE

Example:

if(rsi_handle == INVALID_HANDLE)

{

Print("Failed to create RSI");

}

2.3 Getting RSI Values with CopyBuffer

Conclusion:

RSI values are retrieved with CopyBuffer and handled as an array.

Code example:

double rsi_array[];

ArraySetAsSeries(rsi_array, true);

CopyBuffer(rsi_handle, 0, 0, 2, rsi_array);

Key points:

- [0] is the latest bar, and [1] is the previous bar

- ArraySetAsSeries is required because it reverses the time series order

- Get at least 2 values for cross detection

Common mistakes:

- array out of range

- Not checking the return value of CopyBuffer

- Judging conditions before data has been retrieved

Safety measure:

if(CopyBuffer(rsi_handle, 0, 0, 2, rsi_array) <= 0)

{

return;

}

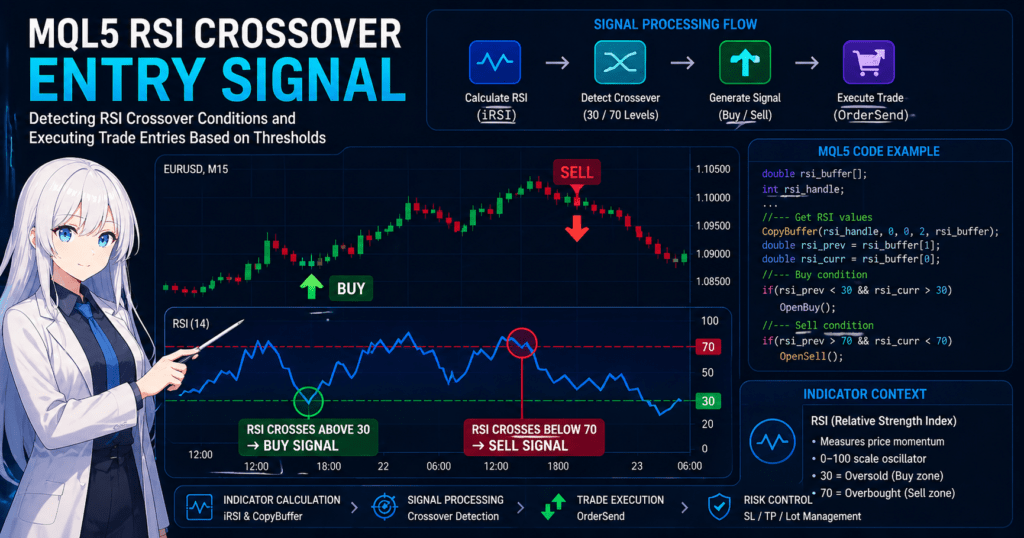

2.4 Implementing Entry Conditions

Conclusion:

Combining RSI thresholds with cross detection can reduce false signals.

Basic conditions:

double rsi_current = rsi_array[0];

double rsi_prev = rsi_array[1];

// Buy (crosses above 30)

if(rsi_prev < 30 && rsi_current > 30)

{

// Buy condition

}

// Sell (crosses below 70)

if(rsi_prev > 70 && rsi_current < 70)

{

// Sell condition

}

Why use crosses?

- A fixed condition such as <30 can trigger repeated entries

- A cross captures a change point

Additional notes:

- A simple strategy based only on RSI < 30 is risky

- Losses can increase during trends

2.5 Order Processing with OrderSend

Conclusion:

Orders are sent by using the MqlTradeRequest structure.

Simple example:

MqlTradeRequest request;

MqlTradeResult result;

ZeroMemory(request);

request.action = TRADE_ACTION_DEAL;

request.symbol = _Symbol;

request.volume = 0.1;

request.type = ORDER_TYPE_BUY;

request.price = SymbolInfoDouble(_Symbol, SYMBOL_ASK);

request.deviation= 10;

OrderSend(request, result);

Important points:

- Consider spread, including the difference between ASK and BID

- Set slippage, or deviation

- Check for execution failure

Failure examples:

- trade context busy

- not enough money

- invalid volume

2.6 Implementation Checklist

Conclusion:

If this checklist is satisfied, you have a minimum RSI EA that can run.

Checklist:

- RSI handle has been created

- CopyBuffer success has been confirmed

- Array errors have been avoided

- Cross conditions are used

- Duplicate entries are prevented by checking positions

- A spread filter is implemented

- Order results are checked

Additional recommendations:

- Control trading hours, such as London session only

- Limit the maximum number of positions

- Adjust lot size

3. How an RSI Strategy Works

Conclusion:

An RSI strategy targets reversals from overextended price movement, also called mean reversion.

Its effectiveness depends on the market environment. It tends to work better in ranging markets, while strong trends can increase losses.

3.1 Why RSI Can Work

Conclusion:

RSI detects a short-term price imbalance and uses the reaction after that imbalance.

RSI is calculated from past upward and downward price movement.

So, when extreme rises or falls continue, the value moves closer to 0 or 100.

This state means the following.

- Buying has become too concentrated, or overbought

- Selling has become too concentrated, or oversold

In markets, this kind of imbalance often does not last for long,

and a correction or rebound in the opposite direction becomes more likely.

This is the basis of an RSI strategy.

Important points:

- RSI is not an indicator that predicts the future

- It quantifies the current overheated state

- Reversals occur only probabilistically and are not guaranteed

3.2 Why RSI Is Strong in Ranging Markets

Conclusion:

When price moves up and down within a fixed range, RSI reversal signals tend to work more easily.

Characteristics of a ranging market:

- No clear trend

- Price movement that goes back and forth

- Relatively stable volatility

In this environment, the following patterns repeat.

- RSI > 70 -> price is more likely to fall

- RSI < 30 -> price is more likely to rise

In other words, RSI’s contrarian logic works directly.

In practice:

- It can be effective on short timeframes such as M5 to M15

- The relative impact of spread is smaller

- The impact of execution delay, or slippage, is also limited

3.3 Why RSI Is Weak in Trending Markets

Conclusion:

In a strong trend, RSI often stops working and repeated losses become more likely.

Characteristics of a trending market:

- Price keeps moving in one direction

- Pullbacks are small

- Momentum is strong

At this point, RSI enters the following state.

- Uptrend -> RSI stays above 70

- Downtrend -> RSI stays below 30

Result:

- Repeated sell trades lose during an uptrend

- Repeated buy trades lose during a downtrend

This is a typical failure pattern.

Common misunderstanding:

- “RSI is 70, so price must fall” -> incorrect

- In reality, it may indicate a strong trend

3.4 Practical Complementary Logic

Conclusion:

RSI alone is not enough. Combining it with filters greatly improves practical usability.

Common complementary methods:

Trend Filter (MA)

- Use a Moving Average

- Allow only buy trades in an uptrend

Example:

if(price > ma && rsi_prev < 30 && rsi_current > 30)

{

// Buy only

}

Effect:

- Avoids countertrend trades against the trend

- Improves win rate

Volatility Filter (ATR)

- Use ATR to check the size of price movement

- Avoid trading when volatility is extremely low or high

Effect:

- Reduces meaningless entries

- Avoids periods when spreads widen

Time Filter (Session)

- Trade only during London and New York sessions

- Avoid low-liquidity periods

Effect:

- Improves execution quality

- Reduces slippage

Risk Management

- Use dynamic adjustment instead of fixed lot size

- Control drawdown, or DD

Reason:

- RSI is a strategy that can produce losing streaks

- Money management often decides whether the strategy survives

Important summary points:

- RSI is not a strategy that wins by itself

- It depends on the environment and is better suited to ranges

- Filters and risk management are essential

4. Differences Between an RSI Strategy and Other Methods

Conclusion:

RSI is simple, reproducible, and contrarian, but it has a clear weakness in trends.

For that reason, it is important to understand how it differs from other methods and use it according to the market environment.

4.1 Method Comparison Overview

Conclusion:

RSI targets reversals from overheated conditions, so its logic is fundamentally different from trend-following methods.

Comparison points:

- Logic, such as contrarian or trend-following

- Strengths, meaning which markets it works in

- Weaknesses, meaning which markets cause it to break down

Typical comparison:

| Method | Logic | Strengths | Weaknesses |

|---|---|---|---|

| RSI | Contrarian | Stable in ranges / easy to implement | Repeated losses in trends |

| Moving Average Cross (MA) | Trend-following | Captures trends | Lag |

| MACD | Hybrid | Trend plus momentum | Many noisy signals |

| Bollinger Bands | Contrarian | Responds to volatility | Depends heavily on settings |

Important points:

- RSI targets reversals

- MA targets continuation

- MACD targets turning points

Because they target different market structures, the issue is not superiority but proper fit.

4.2 Cases Where RSI Is Suitable

Conclusion:

RSI works best in markets where direction is weak and price moves back and forth.

Specific conditions:

- Ranging or sideways market

- Stable volatility

- No clear trend

Characteristics in this situation:

- RSI moves back and forth between 30 and 70

- The overheated-to-reversal pattern repeats

In practice:

- Short timeframes such as M5 to M15

- Highly liquid currency pairs such as EURUSD

- An environment with narrow spreads

Benefits:

- Simple logic means fewer bugs

- The execution impact is relatively small

- Reproducibility is high

4.3 Cases Where Other Methods Have an Advantage

Conclusion:

When a trend is clear, trend-following methods often have higher expected value than RSI.

Cases Where Moving Average (MA) Has an Advantage

- When a strong trend appears

- Markets where buying pullbacks or selling rebounds works

Reason:

- It rides trend continuation

- It uses the opposite idea from RSI contrarian trading

Cases Where MACD Has an Advantage

- The early stage of a trend

- When you want to capture momentum changes

Reason:

- It looks at both trend and momentum

Cases Where Bollinger Bands Have an Advantage

- Markets where volatility changes

- Before and after breakouts

Reason:

- They capture price expansion and contraction

4.4 Practical Strategy Selection

Conclusion:

RSI should not be used alone. Combining it with other methods helps stabilize expected value.

Common combinations:

RSI + MA (Most Important)

- Use MA to judge trend direction

- Use RSI to decide entry timing

Example:

if(price > ma && rsi_prev < 30 && rsi_current > 30)

{

// Buy the pullback during an uptrend

}

Effect:

- Removes countertrend trades against the trend

- Improves win rate

RSI + Volatility Filter

- Use ATR to check price movement

- Exclude low-volatility and high-volatility conditions

Effect:

- Reduces unnecessary trades

- Avoids periods when spreads widen

RSI + Session Control

- Run only during London and New York sessions

- Exclude low-liquidity periods

Effect:

- Stabilizes execution

- Reduces slippage

Important conclusion:

- RSI assumes combination, not standalone optimization

- The advantage changes depending on the market environment

- Strategies should be switched instead of fixed permanently

5. Common Mistakes and Cautions

Conclusion:

Many RSI strategy failures come from misreading the market environment and implementation problems.

The main causes of losses are repeated countertrend trades during trends and ignoring execution conditions such as spread and slippage.

5.1 Risk of Using RSI Alone

Conclusion:

Entries based only on RSI are structurally likely to create repeated losses in trending markets.

Typical patterns:

- Continuing to sell at RSI>70 during an uptrend

- Continuing to buy at RSI<30 during a downtrend

Cause:

- RSI shows overheating, but it does not guarantee a reversal

- Under strong momentum, RSI can stay pinned

Countermeasures:

- Use a trend filter, such as MA

- Use cross conditions, such as crossing above or below a threshold

- Control repeated entries, such as limiting positions in the same direction

Minimum implementation example:

bool HasPosition()

{

return PositionSelect(_Symbol);

}

5.2 Ignoring Spread and Slippage

Conclusion:

Even if a backtest looks good, live performance can worsen because of spread and slippage.

Problems:

- Unfavorable fills when spreads widen, especially around economic news

- Slippage creates a gap from the expected price

- Execution delays can invalidate the signal

Countermeasures:

- Use a spread filter with a maximum allowed value

- Specify deviation, or acceptable slippage

- Trade only during highly liquid sessions

Example:

double spread = (SymbolInfoDouble(_Symbol, SYMBOL_ASK) -

SymbolInfoDouble(_Symbol, SYMBOL_BID)) / _Point;

if(spread > 20) // Example: equivalent to about 2.0 pips

{

return; // Avoid entry

}

5.3 Over-Optimization

Conclusion:

If you adjust parameters such as the RSI period or thresholds too much, the strategy may stop working in future markets.

Common errors:

- Fine-tuning the RSI period from 14 to 13 to 12 and so on

- Adjusting 30/70 too finely, such as 28/72

- Fitting too closely to historical data

Problems:

- Reproducibility disappears

- The strategy breaks down in forward testing

Countermeasures:

- Keep settings simple

- Test across multiple periods to confirm robustness

- Perform walk-forward analysis

5.4 Insufficient Lot Size and Risk Management

Conclusion:

Because RSI strategies can produce losing streaks, poor lot management can quickly reduce account equity.

Typical failures:

- Trading with a fixed lot size

- No stop loss

- No drawdown, or DD, control

Countermeasures:

- Fix risk per trade, such as 1 to 2%

- Set stop losses, such as ATR-based stops

- Set a maximum DD limit, or equity protection

Reference logic:

double risk_percent = 1.0;

double lot = AccountBalance() * risk_percent / 100.0;

*In practice, this must be adjusted based on margin requirements and volatility.

5.5 Mistakes in Data Retrieval and Array Handling

Conclusion:

Mistakes with CopyBuffer or array handling can cause unintended entries or stop the EA.

Common errors:

- array out of range

- Referencing data before CopyBuffer has retrieved it

- Not setting ArraySetAsSeries

Safe implementation:

double rsi_array[];

ArraySetAsSeries(rsi_array, true);

if(CopyBuffer(rsi_handle, 0, 0, 2, rsi_array) <= 0)

{

return;

}

5.6 Lack of Position Management

Conclusion:

Without position management, duplicate entries in the same direction can increase risk exponentially.

Problems:

- Multiple entries from the same signal

- Unintended averaging-down behavior

- Margin pressure, such as not enough money

Countermeasures:

- Check whether a position exists

- Limit the maximum number of positions

- Define close conditions clearly

Important summary points:

- Using RSI alone is risky

- Always consider execution conditions, including spread and slippage

- Over-optimization breaks down over the long term

- Risk management is the top priority

6. Practical Use Cases

Conclusion:

An RSI strategy is not a strategy that wins by itself. It can create more stable expected value when used as part of a portfolio.

It is especially useful as a complementary strategy for ranging markets.

6.1 Using RSI as a Standalone Strategy

Conclusion:

RSI alone is practical only under limited conditions: small lot size, short-term trading, and restricted market conditions.

Suitable conditions:

- A clear ranging market

- Stable volatility

- Narrow-spread currency pairs such as EURUSD

Recommended settings:

- Small lot operation, below 1% of capital

- Short timeframes such as M5 to M15

- Use cross conditions and avoid simple thresholds

Reason:

- RSI can easily produce losing streaks

- Standalone operation is high risk because it breaks down in trends

Practical positioning:

- A secondary strategy or test strategy

- Often not suitable as the main logic

6.2 Combining RSI with Other Strategies

Conclusion:

RSI is most effective when used as an entry timing tool.

Common combinations:

RSI + Moving Average (Most Important)

Role division:

- MA: judge trend direction

- RSI: time the entry

Example:

if(price > ma && rsi_prev < 30 && rsi_current > 30)

{

// Buy the pullback

}

Effect:

- Removes countertrend trades against the trend

- Improves win rate and stability

RSI + ATR (Volatility Control)

Role:

- Use ATR to judge the size of price movement

- Exclude low-volatility and high-volatility environments

Effect:

- Reduces meaningless entries

- Reduces slippage risk

RSI + Session Filter

Role:

- Limit trading hours

- Avoid low-liquidity periods

Examples:

- London session

- New York session

Effect:

- Improves execution quality

- Avoids spread widening

6.3 Recommended Practical Operating Model

Conclusion:

The most realistic approach is to include RSI as part of a strategy portfolio.

Recommended model:

- Trend strategy, such as MA-based logic

- Contrarian strategy, such as RSI

- Volatility strategy, such as ATR-based logic

In this way, multiple strategies are combined.

Reason:

- Markets are always changing

- A single strategy depends heavily on the environment

6.4 How to Diversify Drawdown

Conclusion:

Because RSI loses during trends, combining it with other strategies can diversify DD.

Example:

| Market | RSI | Trend Strategy |

|---|---|---|

| Range | Profit | Small loss |

| Trend | Loss | Profit |

This structure can produce the following benefits:

- More stable overall profit and loss

- A smoother equity curve

6.5 Key Points for Practical Use

Conclusion:

When using RSI in practice, market awareness and risk control are the most important points.

Checklist:

- Is the current market ranging or trending?

- Is the spread within the acceptable range?

- Is this a time when slippage is likely to occur?

- Are positions becoming excessive?

If these are ignored, the result can be:

- A large gap from the backtest

- Unexpected losses

Important summary:

- RSI is unstable by itself

- Its value appears when combined with other logic

- Portfolio design is the premise

7. Frequently Asked Questions (FAQ)

Conclusion:

An RSI strategy is simple, but results change greatly depending on settings, usage, and market environment.

The FAQ below gives direct answers to common practical questions.

7.1 What Is the Best RSI Period?

Conclusion:

The standard period is generally 14, but the best value changes by currency pair, timeframe, and market environment.

Additional notes:

- Short period, such as 7 to 10: faster response but more noise

- Long period, such as 20 to 30: more stable but creates lag

In practice:

- Start testing with 14

- If changing it, make a meaningful change, such as 14 to 21

7.2 Can RSI Be Used Alone?

Conclusion:

Standalone use is not recommended. Combining it with a trend filter should be the basic assumption.

Reason:

- It can suffer repeated losses in trending markets

- It produces many false signals

Recommended combinations:

- RSI + MA, the most important combination

- RSI + ATR

7.3 Are RSI 30/70 Levels Fixed?

Conclusion:

They are not fixed and can be adjusted according to the market.

Examples:

- High volatility -> 20 / 80

- Narrow range -> 40 / 60

However:

- Excessive adjustment can cause overfitting

7.4 What Is the Difference Between RSI and MACD?

Conclusion:

RSI is a contrarian indicator, while MACD is closer to a trend-based indicator.

Differences:

- RSI: overheated condition, oscillator

- MACD: trend plus momentum

How to use them:

- Range -> RSI

- Trend -> MACD

7.5 In What Markets Does RSI Not Work?

Conclusion:

RSI does not work well in strong trending markets.

Characteristics:

- RSI stays pinned above 70 or below 30

- Price does not reverse

Countermeasures:

- Judge the trend first

- Add filters

7.6 Is Backtesting Enough?

Conclusion:

No. Forward testing is always required.

Reason:

- Execution conditions such as spread and slippage are not fully reproduced

- There is a risk of over-optimization

Recommended:

- Test with a demo account

- Run live-environment tests on a VPS

7.7 Can RSI Be Used for Scalping?

Conclusion:

Yes, but costs such as spread and slippage have a very large impact.

Cautions:

- Wide spreads can eliminate profit

- Execution delays can break the entry condition

Countermeasures:

- Use a low-spread account

- Use a fast execution environment

7.8 Is RSI or Bollinger Bands Better?

Conclusion:

Neither is simply better. They serve different purposes.

Differences:

- RSI looks at overheated conditions

- Bollinger Bands look at price distribution

In practice:

- They are often used together

Important summary:

- RSI results change depending on settings and environment

- Combination is usually the premise, rather than standalone use

- The validation process is the most important part