- 1 1. What Is EA Performance Optimization?

- 2 2. Practical Steps for EA Performance Optimization

- 3 3. How EA Performance Optimization Works

- 4 4. Comparison of EA Performance Optimization Methods

- 5 5. Common EA Performance Optimization Mistakes and Precautions

- 6 6. Practical Use Cases for EA Performance Optimization

- 6.1 6.1 Optimization During New EA Development

- 6.2 6.2 Improving an Existing EA

- 6.3 6.3 Optimization When Running Multiple EAs

- 6.4 6.4 Timing for Re-Optimization During Operation

- 6.5 6.5 Relationship with Broker and VPS Selection

- 6.6 6.6 Relationship Between Risk Management and Optimization

- 6.7 6.7 Simple Optimization Rules for Practice

- 7 7. Frequently Asked Questions About EA Performance Optimization

- 7.1 7.1 Is EA Optimization Always Necessary?

- 7.2 7.2 How Much Can Backtest Results Be Trusted?

- 7.3 7.3 Should the Optimal Parameter Be a Single Value?

- 7.4 7.4 What PF Level Is a Practical Guide?

- 7.5 7.5 How Long Should Forward Testing Run?

- 7.6 7.6 How Much Do Demo and Live Account Differences Matter?

- 7.7 7.7 How Often Should Optimization Be Performed?

- 7.8 7.8 Is a VPS Required?

1. What Is EA Performance Optimization?

Conclusion:

EA performance optimization is not about “maximizing profit.” It is a tuning process for stabilizing reproducible returns while controlling risk.

Its core purpose is not simple optimization, but designing a balance that can survive live trading conditions.

1.1 Definition of EA Performance Optimization

Definition:

EA performance optimization means adjusting multiple factors such as spread, slippage, execution, trading logic, and parameters to optimize the balance between risk and return.

Many beginners misunderstand optimization as “maximizing profit in a backtest,” but that is a typical path into over-optimization, also called overfitting.

The key points to evaluate are:

- Evaluate not only PF (profit factor), but also DD (drawdown)

- Check whether performance is stable across multiple periods, not only one selected period

- Confirm whether the EA can tolerate wider spreads and execution delays

- Confirm whether results can be reproduced in a live environment

In short, EA optimization is the process of tuning an EA based on whether it can still work in the future.

1.2 Why Optimization Is Necessary

Conclusion:

Because market conditions constantly change, an EA that is not optimized will usually lose performance over time.

The foreign exchange market includes changing factors such as:

- Volatility, or the size of price movement

- Spread changes, especially around economic releases

- Execution latency

- Changes in liquidity

For example, even an EA that performs well in a backtest can lose much of its expectancy if:

- The spread widens from 1.0 to 2.5

- Slippage of +0.3 pips occurs

This is especially noticeable with scalping EAs.

1.3 Main Elements to Optimize

Conclusion:

EA optimization is not enough if it only adjusts parameters. It requires an overall design that includes the execution environment.

The main optimization targets are as follows:

Logic and Parameters

- Entry conditions, such as indicator thresholds

- Exit conditions, such as TP/SL and trailing stops

- Lot size and money management

Execution Environment

- VPS for a low-latency environment

- Broker selection based on spread and execution quality

- Server distance and latency

Trading Cost Factors

- spread

- slippage

- commission

Filters and Avoidance Logic

- Avoiding major economic news releases

- Time-of-day filters

- Stopping trades during high-spread conditions

1.4 Common Beginner Misunderstandings

Conclusion:

The biggest trap is assuming that “the setting with the highest profit is the optimal setting.”

Common misunderstandings include:

- Choosing the setting with the highest backtest profit

- Judging an EA as good only because its PF is high

- Testing only one period

- Trusting demo results too much

The following are especially dangerous:

- Adjusting parameters too finely, which leads to over-optimization

- Creating settings that only fit one specific market condition

- Watching the EA fail during forward testing

This means the EA has only adapted to the past and has no real generality for the future.

1.5 Practical Role in the Development Workflow

Conclusion:

EA optimization is not the final step of development. It is part of the validation loop.

In practice, it is used in this flow:

- Logic design

- Initial backtest

- Optimization, or parameter tuning

- Forward test on demo

- Live validation with small lots

- Re-optimization when necessary

The important points are:

- It is not a one-time task

- It should be repeated when the environment changes

- It must be validated with live data

In other words, EA optimization is a continuous adjustment process.

2. Practical Steps for EA Performance Optimization

Conclusion:

EA optimization should be done step by step in the order of backtesting, parameter search, forward validation, and live trading tests. This helps secure reproducibility and stability.

2.1 Overall Optimization Flow

Conclusion:

Optimization is not something completed in one attempt. It is a process of improving accuracy in stages.

The basic flow is:

- Check basic performance with a backtest

- Extract parameter candidates through optimization

- Verify reproducibility with forward testing

- Test in a live environment with small lots

- Adjust again if necessary

Following this flow helps avoid over-optimization and overfitting.

2.2 How to Run Backtests Correctly

Conclusion:

Backtests should be configured with priority on accuracy and realism.

Steps

- Use tick data, preferably real ticks when available

- Set the spread to a realistic value instead of a fixed ideal value

- Account for slippage

- Use multiple years, ideally at least 3 to 5 years

- Include different market types, such as trends and ranges

Example in MQL5: Strategy Tester Settings Concept

// Spread consideration (pseudo)

input double Spread = 1.5;

// Slippage tolerance

input int Slippage = 3;

// On order placement

trade.Buy(lot, _Symbol, Ask, Slippage, sl, tp);

Common Mistakes

- Testing with a spread of 0 or a fixed unrealistic value

- Evaluating only a short period, such as a few months

- Ignoring execution latency

Reason:

In live trading, transaction costs reduce profit. Ignoring them distorts the results.

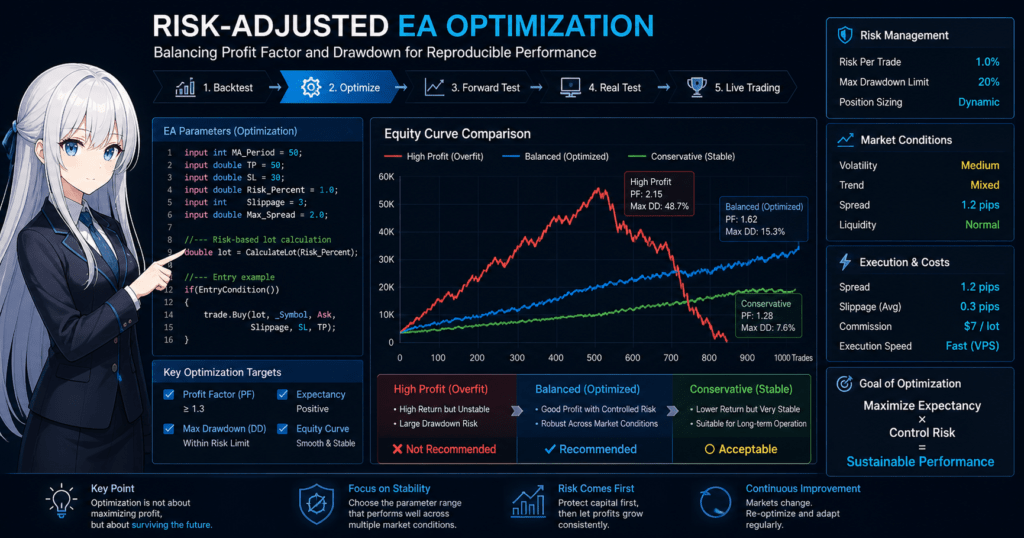

2.3 How to Proceed with Parameter Optimization

Conclusion:

Parameters should be searched “broadly and roughly,” not “narrowly and deeply.” The goal is to find stable zones.

Steps

- Select target parameters, such as MA period or TP/SL

- Set a wide search range

- Use rough step sizes to reduce over-optimization

- Compare multiple good results

Example: MQL5 Input Parameters

input int MA_Period = 50; // Optimization target

input double TP = 50;

input double SL = 30;

Evaluation Criteria

- PF, with 1.3 or higher as a rough guide

- Maximum drawdown within the acceptable range for the account

- Expectancy rather than win rate

- Smoothness of the equity curve

Common Mistakes

- Choosing only the single result with the highest profit

- Making parameter steps too fine

- Ignoring variation among results

Key point:

Choose a stable range, not a peak.

2.4 Validation with Forward Testing

Conclusion:

Backtest results are only a hypothesis. An EA’s usefulness is confirmed only through forward testing.

Steps

- Run the EA on a demo account

- Continue for at least 1 to 3 months

- Compare under the same conditions as the backtest

- Check execution quality

Items to Check

- Impact of spread

- Frequency of slippage

- Whether re-quotes occur

- Unexpected drawdown

Common Mistakes

- Making a decision after too short a period

- Trusting demo results too much

- Ignoring differences from live trading

Reason:

A demo environment may provide more favorable execution than live trading.

2.5 Final Validation in a Live Environment

Conclusion:

The final decision must be made on a live account.

Steps

- Start with small lots

- Check differences from demo trading

- Record costs, including spread and slippage

- Observe for several weeks to several months

Checkpoints

- Actual execution quality

- Impact of VPS latency

- Broker-specific behavior

Common Mistakes

- Starting with large lots immediately

- Believing demo results without adjustment

- Stopping after a short-term result

2.6 Practical Optimization Tips

Conclusion:

Optimization is usually more effective over the long term when it prioritizes a design that does not break, rather than an aggressive design.

Important practical ideas include:

- Create times when the EA does not trade by using filters

- Stop trading when spreads are high

- Avoid major economic releases

- Keep lot size controlled for drawdown management

Note:

Strong EAs are clear about when they should not trade.

3. How EA Performance Optimization Works

Conclusion:

The essence of EA optimization is using past data to build resistance against future uncertainty. It is not just tuning. It is a matter of probability and structure.

3.1 Why Backtesting Alone Is Not Enough

Conclusion:

A backtest is a fit to the past, not a guarantee for the future. For that reason, it cannot be trusted by itself.

Backtesting has limits:

- The EA becomes optimized to past data, which can cause overfitting

- Spread and slippage may be idealized

- Execution latency may not be reflected

Example:

- Backtest: PF 1.8

- Live trading: PF drops below 1.2

This can happen because of:

- Wider spread

- Increased slippage

- Order rejection

In short, a backtest is a hypothesis-generation tool. It is not something that should be used for live trading without further validation.

3.2 The Structure of Over-Optimization

Conclusion:

Over-optimization means the EA has adapted even to noise. It is one of the most common failure patterns.

How it happens:

- Parameters are adjusted too finely

- The settings match price movement in one specific period

- Generality disappears

Typical example:

- The best result appears when the MA period is set to 47

- But the setting does not work in other periods

This is not a meaningful edge. It is only coincidence.

How to Detect It

- Shift the parameter slightly, such as from 47 to 45 or 50

- If performance drops sharply, the setting is risky

The important idea is:

- Good settings are stable across a broad range

- Bad settings stand out at only one point

3.3 Relationship Between Market Regime Changes and EA Performance

Conclusion:

EA performance depends on the market regime, so fixed optimization will not keep working forever.

Main changing factors include:

- Trending markets versus ranging markets

- High or low volatility

- Interest rate policy and economic indicators

- Liquidity, since lower liquidity often increases slippage

Examples:

- A trend-following EA may lose more in a range

- A scalping EA may fail when spreads widen

Therefore, optimization should assume the following:

- Include multiple market conditions

- Design the EA so it does not depend on one specific environment

3.4 Designing the Balance Between Expectancy and Risk

Conclusion:

Optimization should focus on expectancy multiplied by risk management, not maximum profit.

Important metrics include:

- Expectancy

- PF, or profit factor

- Maximum drawdown, or DD

- Win rate as a secondary reference

The basic judgment is:

- High profit with large DD should be rejected

- Moderate profit with stability can be adopted

A Simple Way to Think About Expectancy

- Win rate x average profit – loss rate x average loss

The important requirements are:

- The result must be reproducible

- The strategy must not collapse

3.5 Impact of Execution and Cost

Conclusion:

EA performance can change more because of the execution environment than because of the trading logic itself.

Influencing factors include:

- spread

- slippage

- execution speed

Example:

- +0.5 pips of slippage

This can be fatal for scalping.

Why It Matters

Because an EA trades mechanically:

- It cannot avoid bad conditions by human discretion

- It directly absorbs worsening execution conditions

For that reason, practical measures are needed, such as:

- Using a VPS to reduce latency

- Selecting a low-spread broker

- Prioritizing execution quality

3.6 Why the Decision Not to Trade Is Important

Conclusion:

The essence of optimization is not deciding where to win. It is deciding where not to lose.

Important avoidance conditions include:

- During economic releases, when volatility can surge

- When spreads widen

- During low-liquidity periods, such as early market hours

The reasons are:

- To avoid situations where expectancy breaks down

- To remove unfavorable trading conditions

In practice, this means:

- Adding filters

- Reducing trade frequency

- Removing unnecessary entries

The result is:

- Improved PF

- Lower DD

- Better stability

4. Comparison of EA Performance Optimization Methods

Conclusion:

EA optimization has several methods, and each differs in accuracy, reproducibility, and risk tolerance. It is important to use methods based on purpose instead of relying on only one.

4.1 Main Optimization Methods

Conclusion:

Optimization methods can be grouped into search methods, validation methods, and adaptive methods.

| Method | Overview | Characteristics |

|---|---|---|

| Grid search | Searches all parameter combinations | Comprehensive, but prone to over-optimization |

| Genetic algorithm | Searches efficiently for an optimal solution | Fast, but may lean toward local optima |

| Walk-forward analysis | Splits periods for optimization and validation | Close to live trading evaluation |

| Monte Carlo analysis | Adds random variation | Can evaluate risk tolerance |

| Forward test | Validates in real time | Closest to real trading |

4.2 Grid Search vs. Genetic Algorithm

Conclusion:

Use grid search when accuracy matters most, and use a genetic algorithm when efficiency matters most.

Comparison Points

| Factor | Grid Search | Genetic Algorithm |

|---|---|---|

| Accuracy | High, because it searches all combinations | Medium, because it uses approximate solutions |

| Computational cost | Very high | Low |

| Over-optimization risk | High | Medium |

| Practical fit | Better for small-scale testing | Better for large-scale optimization |

Practical Judgment

- Initial validation: use a rough grid search

- Full-scale optimization: use a genetic algorithm

Important note:

Both depend on past data, so neither is sufficient by itself.

4.3 Importance of Walk-Forward Analysis

Conclusion:

Walk-forward analysis is the most practical method for evaluating future reproducibility.

Overview

- Optimize in Period A

- Validate in Period B

- Repeat the process

Advantages

- Can detect over-optimization

- Allows evaluation close to live trading

- Can check resistance to market changes

Disadvantages

- Settings are complex

- Calculation time is long

In practice:

- Even a simplified version is highly worth using

4.4 Risk Evaluation with Monte Carlo Analysis

Conclusion:

Monte Carlo analysis is a method for understanding worst-case scenarios.

What It Does

- Randomizes trade order

- Adds random slippage

- Simulates variation in profit and loss

What You Can Learn

- Distribution of maximum drawdown

- Risk of ruin

- Stability

Why It Matters

A backtest shows only one result.

Monte Carlo analysis visualizes the range of possible outcomes.

4.5 Difference from Forward Testing

Conclusion:

Forward testing is the only method that can collect data close to real trading conditions.

| Item | Backtest | Forward Test |

|---|---|---|

| Data | Past | Current and ongoing |

| Reproducibility | Low | High |

| Speed | Fast | Slow |

| Reliability | Hypothesis | Evidence |

The important point is:

- Backtest: hypothesis generation

- Forward test: validation

4.6 Which Method Should You Choose?

Conclusion:

The best answer is not one method. It is a combination of methods.

Recommended Flow

- Grid search or genetic algorithm for rough search

- Walk-forward analysis to confirm reproducibility

- Monte Carlo analysis for risk evaluation

- Forward testing for final validation

Decision Criteria

- If time is limited, focus on genetic algorithms

- If accuracy matters, combine grid search and walk-forward analysis

- If stability matters, Monte Carlo analysis is essential

4.7 Common Mistakes in Method Selection

Conclusion:

The most common mistake is making a decision based on only one method.

Typical examples include:

- Adopting an EA based only on a backtest

- Using genetic algorithm results without validation

- Starting live operation without forward testing

The result can be:

- Failure in live trading

- Sharp increase in DD

- Loss of expectancy

5. Common EA Performance Optimization Mistakes and Precautions

Conclusion:

Most EA optimization failures come down to fitting too closely to the past and ignoring live trading costs. If these points are missed, even strong trading logic can fail in live trading.

5.1 Over-Optimization

Conclusion:

The most common failure is adopting settings that perfectly fit one specific period.

Typical examples include:

- Continuing to fine-tune parameters

- Adopting one backtest result that looks extremely good

- Finding that the setting does not work in other periods

How to Identify It

- Performance drops sharply when parameters are changed slightly

- The equity curve looks unnaturally smooth

- PF is unusually high, such as 2.5 or higher

Countermeasures

- Use wider step sizes

- Compare multiple good patterns

- Use walk-forward analysis together with optimization

Reason:

Choosing a stable zone increases resistance to future changes.

5.2 Underestimating Spread and Slippage

Conclusion:

If trading costs such as spread and slippage are ignored, profit can disappear easily in live trading.

Common mistakes include:

- Backtesting with a spread of 0

- Ignoring slippage

- Evaluating based on demo conditions

The impact is especially large for:

- Scalping EAs

- High-frequency trading

- Low-TP settings

Countermeasures

- Set spread to live values plus a buffer

- Test with assumed slippage

- Compare differences among brokers

5.3 Judging from Short Test Periods

Conclusion:

Short-term results are heavily affected by chance and are not enough for judgment.

Typical examples include:

- Adopting an EA after one month of forward testing

- Evaluating only one specific market condition

- Judging only during a trend period

Problems

- The sample may include market bias

- Drawdown may not have occurred yet

- The risk is not visible

Countermeasures

- Use at least 3 to 6 months of forward testing

- Include multiple market conditions

- Observe until drawdown occurs

5.4 Overtrusting Demo Accounts

Conclusion:

Demo results are useful as a reference, but trusting them as-is is risky.

The reasons are:

- Execution is often more favorable

- Slippage is often lower

- Execution can be too stable

A common misunderstanding is:

- If it wins on demo, it will win on live

Countermeasures

- Validate on a live account with small lots

- Record differences from demo results

- Compare execution quality

5.5 Ignoring Lot Management

Conclusion:

A lot size mistake can destroy the account before optimization even matters.

Typical examples include:

- Taking excessive risk with fixed lots

- Ignoring DD

- Ignoring the impact of losing streaks

Countermeasures

- Limit risk per trade, such as 1% to 2%

- Calculate lot size backward from maximum DD

- Consider correlation when using multiple EAs

5.6 Missing Filters and Avoidance Logic

Conclusion:

An EA that does not avoid loss-prone conditions will eventually break down over the long term.

Uncovered cases include:

- Rapid rises and falls during economic releases

- Sudden spread expansion

- Low-liquidity time periods

Countermeasures

- Time-of-day filters

- Spread filters

- Economic news avoidance logic

Reason:

Because an EA cannot make discretionary judgments, bad conditions must be excluded in advance.

5.7 Misunderstanding Evaluation Metrics

Conclusion:

Using a single metric leads to poor optimization decisions.

Common mistakes include:

- Judging only by PF

- Focusing only on win rate

- Looking only at total profit

Correct Evaluation

- Combine PF, DD, and expectancy

- Check equity curve stability

- Verify live reproducibility

5.8 Practical Checklist

Conclusion:

After optimization, using a checklist can greatly reduce risk.

Check the following:

- Is performance stable across multiple periods?

- Can the EA tolerate spread changes?

- Was slippage considered?

- Was performance reproduced in forward testing?

- Is DD within the acceptable range?

- Has the EA been validated live?

6. Practical Use Cases for EA Performance Optimization

Conclusion:

EA optimization is not only a development task. It is a practical process connected to operation, improvement, and money management. Used properly, it can improve both return stability and risk control.

6.1 Optimization During New EA Development

Conclusion:

Optimization becomes much more accurate when it is built into the design stage instead of being added after the logic is complete.

Practical workflow:

- Design the logic as a hypothesis

- Confirm direction with a backtest

- Use rough optimization to identify parameter ranges

- Design filters for time, spread, and news events

- Retest

Important Points

- Do not optimize finely from the beginning

- Do not postpone filter design

- Define “do not trade” conditions early

Reason:

Adding filters later can break the logic.

6.2 Improving an Existing EA

Conclusion:

When an EA’s performance worsens, it is often improved by optimizing the environment rather than changing the logic.

Improvement approaches include:

- Reviewing spread conditions

- Adding time-of-day filters

- Adjusting lot size

- Moving to a VPS for lower latency

Specific Examples

- A scalping EA improves after adding spread limits

- A trend-following EA reduces DD through time control

Common Mistakes

- Rebuilding the logic immediately

- Continuing to make tiny parameter changes

In practice:

- Review in the order of environment, filters, then parameters

6.3 Optimization When Running Multiple EAs

Conclusion:

When running multiple EAs, portfolio optimization matters more than optimizing each EA in isolation.

Factors to consider include:

- Diversification across currency pairs, such as EURUSD and USDJPY

- Diversification across logic types, such as trend-following and countertrend

- Diversification across trading times

- Correlation to avoid simultaneous losses

Specific Measures

- Avoid running multiple versions of the same logic

- Choose combinations whose DD does not overlap heavily

- Manage lot size at the portfolio level

Common Mistakes

- Each EA looks strong individually, but they fail at the same time

- Trades concentrate in the same currency pair and time period

The result can be:

- DD expands more than expected

6.4 Timing for Re-Optimization During Operation

Conclusion:

Re-optimization is more reasonable when based on anomaly detection, not on a fixed schedule.

Criteria for re-optimization include:

- PF declines, such as from 1.3 to 1.0 or lower

- DD increases sharply

- The execution environment changes

- The market regime changes

Recommended Decision Flow

- Temporary weakness: continue observing

- Clear deterioration: re-optimize

- Structural change: review the logic

Important Notes

- Frequent re-optimization can be counterproductive

- Do not react to noise

6.5 Relationship with Broker and VPS Selection

Conclusion:

EA performance can change greatly depending on the broker and VPS, so they should be considered together with optimization.

Important factors include:

- Spread, where lower is generally better

- Execution quality, including speed and slippage

- Server distance and latency

Practical Actions

- Compare tests across multiple brokers

- Place the VPS near the trading server

- Analyze execution logs

Common Mistakes

- The EA breaks after changing brokers

- Latency occurs because no VPS is used

6.6 Relationship Between Risk Management and Optimization

Conclusion:

Optimization should be used to avoid account failure, not to maximize profit.

Important ideas include:

- Lower DD is more favorable over the long term

- Lower lot size increases survival probability

- Expectancy matters more than win rate

Example Practical Rules

- Limit maximum DD to 20% or less

- Risk 1% to 2% per trade

- Adjust lot size during losing streaks

6.7 Simple Optimization Rules for Practice

Conclusion:

Even without complex methods, simple rules can provide enough optimization for many practical cases.

Simple rules:

- Set parameters roughly

- Use PF 1.3 or higher as a reference

- Prioritize DD when choosing settings

- Require forward testing

- Make the final decision in live trading

Following these five points can avoid most major failures.

7. Frequently Asked Questions About EA Performance Optimization

Conclusion:

Most questions about EA optimization focus on how much to trust the results and which methods to use. Clear decision criteria are essential.

7.1 Is EA Optimization Always Necessary?

Conclusion:

Yes, it is necessary. However, it should not be overdone.

If optimization is not performed:

- The EA cannot respond to market changes

- Performance can deteriorate

On the other hand, over-optimization is counterproductive.

In many cases, rough adjustment and stability checks are enough.

7.2 How Much Can Backtest Results Be Trusted?

Conclusion:

Backtests should be treated as a reference or hypothesis. They cannot be trusted alone.

A rough reliability guide is:

- Backtest: low, because it is a hypothesis

- Forward test: medium, because it validates the hypothesis

- Live trading: high, because it provides evidence

The important checks are:

- Whether the result matches forward testing

- Whether execution conditions are realistically reproduced

7.3 Should the Optimal Parameter Be a Single Value?

Conclusion:

No. It is better to choose a stable range instead of one exact value.

The reasons are:

- Markets change, so fixed values can fail

- Peak values are more likely to be over-optimized

In practice:

- Identify a good parameter range

- Use a middle value within that range

7.4 What PF Level Is a Practical Guide?

Conclusion:

For live trading, PF around 1.2 to 1.5 is a realistic range.

Rough guide:

- PF below 1.0: reject

- PF 1.2 to 1.5: practical level

- PF 2.0 or higher: possible over-optimization

The important point is:

- Balance PF with DD instead of judging by PF alone

7.5 How Long Should Forward Testing Run?

Conclusion:

At least 1 to 3 months is needed, and 6 months or longer is preferable when possible.

The reasons are:

- To reduce market bias

- To confirm drawdown

With a short test period:

- You may fail to notice a lucky winning streak

7.6 How Much Do Demo and Live Account Differences Matter?

Conclusion:

They matter a lot, especially for scalping.

Main differences include:

- slippage, which is usually larger in live trading

- execution, which is usually more stable on demo

- spread fluctuation

Therefore:

- Do not trust demo results as-is

- Always validate in live trading

7.7 How Often Should Optimization Be Performed?

Conclusion:

Optimization should be performed when performance deteriorates, not on a fixed schedule.

Useful signs include:

- PF decline

- DD increase

- Market condition changes

Optimizing too frequently can:

- Adapt the EA to noise

- Make performance unstable

7.8 Is a VPS Required?

Conclusion:

For short-term trading such as scalping, a VPS is almost essential.

The reasons are:

- Reduced execution delay

- Lower slippage risk

- Stable operation

For medium- to long-term EAs, a VPS may not always be required.

However, it is recommended when operational stability matters.